In the week ended 3rd July, 2020, that saw the end of the second quarter, and ushered in the third quarter of the year, Investors in the Nigerian Stock Exchange endured a loss of N257.12 billion, with the market index declining by 1.99%.

The YTD performance worsened to minus 9.34%, as the All Share Index settled at 24,374.40 and Market Capitalization at N12.69 trillion.

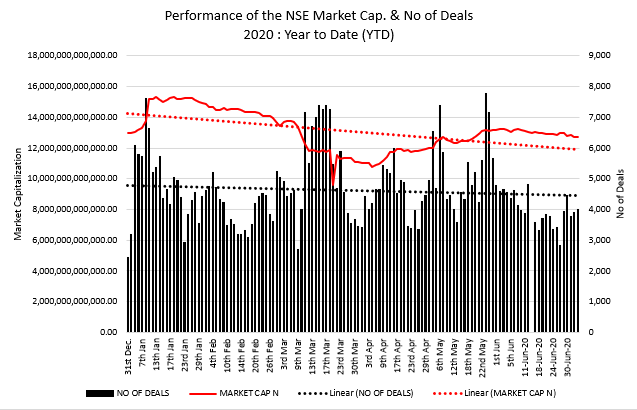

A total turnover of 961.833 million shares worth N9.181 billion in 20,058 deals were traded this week by investors on the floor of the Exchange, in contrast to a total of 739.375 million shares valued at N8.563 billion that exchanged hands last week in 17,248 deals.

- Read also; Dangote Cement Plc to commence closed period from July 8, 2020

- Guaranty Trust Bank Plc declares closed period for H1 financial report

The activity level improved, as volume of shares traded increased by 30.0% while the value of stocks traded increased by 7.2%. Overall, our chart of activity level shows that the trend of volume and value of traded stocks continued downwards.

The Financial Services industry (measured by volume) led the activity chart with 457.851 million shares valued at N3.773 billion traded in 8,062 deals; thus contributing 61.92% and 44.06% to the total equity turnover volume and value respectively.

Trading in the top three equities namely FBN Holdings Plc, Guaranty Trust Bank Plc and United Bank for Africa Plc. (measured by volume) accounted for 275.099 million shares worth N2.818 billion in 3,497 deals, contributing 28.60% and 30.69% to the total equity turnover volume and value respectively.

The number of deals being done by market participants is moving downwards, albeit with a fairly constant trend line.

Of the 5 indices under our watch, only two have a positive performance YTD.

- Insurance Index: +0.63%

- Oil & Gas Index: -25.26%

- Banking Index: -25.02%

- Consumer Goods Index: -27.33%

- Industrial Goods Index: +3.95%

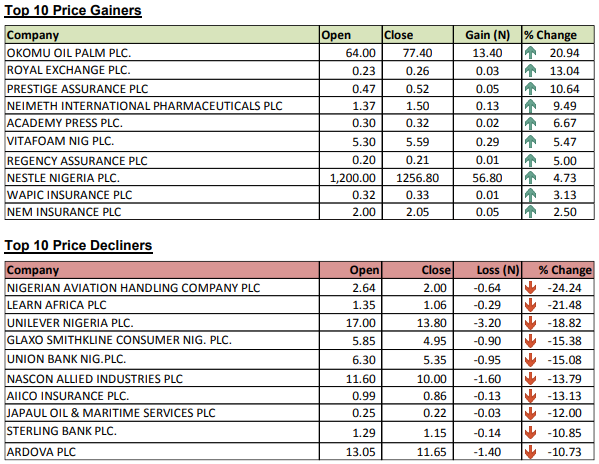

Thirteen (13) equities appreciated in price during the week, lower than Eighteen (18) equities in the previous week. Fifty-nine (59) equities depreciated in price, higher than Forty-three (43) equities in the previous week, while ninety-one (91) equities remained unchanged, lower than One- hundred and two (102) equities recorded in the previous week.

The top gainers and losers in the week are as tabulated below;

Data source; NSE

Companies has started announcing closed periods and dates for board meetings in preparation for the release of the H1 financial results for the period ended 30th June, 2020, Investors will be watching to see the impact of the COVID-19 pandemic on the performance of the listed companies.

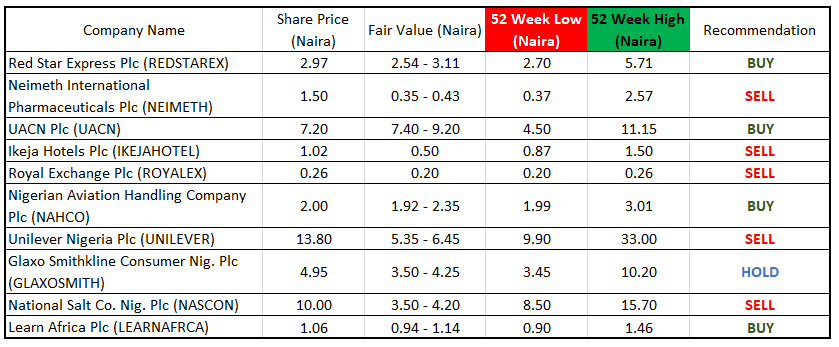

Stock Pick for the week ahead

With 4 out of our 10 stock picks bagging a BUY recommendation, it portrays the gradual opening up of attractive entry positions for Investors. REDSTAREX, UACN, NAHCO, and LEARNAFRCA are all consistent dividend stocks, at current prices are poised to return a dividend yield of over 10% for the financial year. An indication on the potential yield will depend on the forthcoming result, that will show the extent of the impact of the pandemic on these companies.

GLAXOSMITH is very close to the fair value calculated by Analyst’s at Investogist, and is expected to break into the range in the next week of trading. However, we have been of the opinion that GLAXOSMITH will return good value for medium to long term Investors, given the Government’s support to Pharmaceutical companies and the role the parent company is playing in the search for COVID-19 vaccine. When the stock price falls within the fair value range, it will become a BUY for us.

Three of the five stocks with a SELL rating have none or little dividend history, the rise and fall of their share prices appear to be driven by sentiments, thus making them very good JIJO (Jump In Jump Out) stocks.

UNILEVER and NASCON have been under performing in recent years, and their dividend payouts has been decreasing along with their valuations. Although a reversal of their fortunes should see an upward revision of their fair values, for now, they remain a SELL.

Written by;

Nnamdi M.

{kind=link}