The Bears held the floor in the first three trading sessions on the floor of the Nigerian Stock Exchange (NSE), in the week ended 11th September, 2020.

Having closed trading in the preceding week at 25,582.23 points, the NSE All-Share Index dropped to 25,582.23 on Monday, then to 25,497.32 on Tuesday and on Wednesday it closed at 25,424.91 points.

The decline was caused primarily by an unprovoked sell-off of Banking stocks, following the release of the long awaited Half Year financial statements of the top tier 1 banks; ZENITHBANK, GUARANTY, ACCESS, UBA and STANBIC.

- Read also: Big tech selloff drags Nasdaq to worst week in months

- Enroll your business with Youth MSMEs database for opportunities including up to N50mn loan at 5% rate

The negative trend was reversed on Thursday, with the NSE ASI closing at 25,520.97 on Thursday, and 25,591.95 on Friday.

Ironically, the rally upwards was also led by the banking stocks, as Investors took advantage of the declining share prices to position for interim dividends.

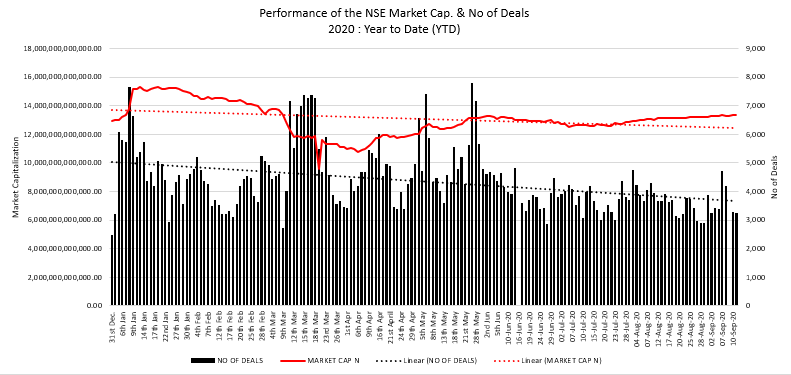

The Thursday and Friday rallies were not sufficient to reverse the loses suffered in the first three days of trading in the week, thus, the All-Share Index lost 0.05% in the week, with Market Capitalization decreasing by N7.143 billion to settle at N13.350 trillion.

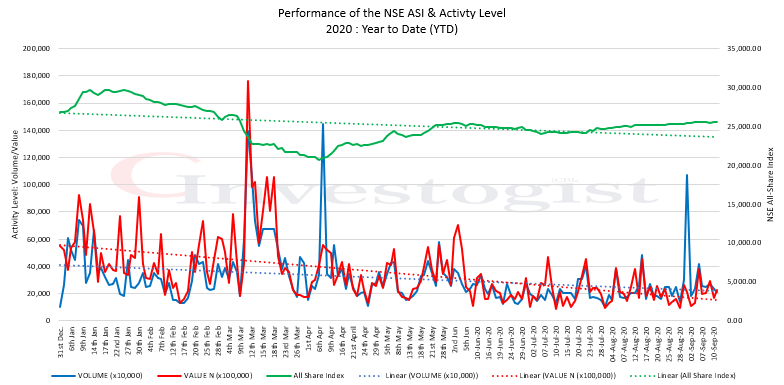

The activity level waned last week, as the total volume and value of shares traded in the week decreased by 44.44% and 0.79% respectively.

A total turnover of 1.22 billion shares worth N10.87 billion in were traded this week by investors on the floor of the Exchange, in contrast to a total of 2.20 billion shares valued at N10.95 billion that exchanged hands last week.

The activity chart shows a return to the depressed activity level in the market, as the trend of volume and value of traded shares turned downwards again after the uptick in the preceding week.

At the end of trading on Friday, 11th September, the NSE ASI was down by 4.66%. The YTD Performances of the 5 indices under our watch are;

- Insurance Index: +6.59%

- Industrial Goods Index: +4.89%

- Banking Index: -17.62%

- Oil & Gas Index: -26.96%

- Consumer Goods Index: -27.10%

4 out of the 5 indices closed the week in negative territory, while 1 advanced. The Industrial Goods Index advanced by 0.35% driven by gains in WAPCO (+6.7%).

The Banking and Oil & Gas indices declined by -2.69% and -1.25% respectively, on the back of loses recorded by UBA (-3.39%) and ZENITHBANK (-1.1%) for banking index and SEPLAT (-2.5%) for the Oil & Gas index.

The Insurance and Consumer Goods indices shed 0.66% and 0.27% respectively, as CORNERSTONE lost 1.5%, DANGSUGAR (-3.6%) and VITAFOAM (-4.9%).

Investor sentiment as measured by market breadth (advance/decline ratio) weakened to 0.7x from the 2.2x recorded last week as 23 stocks gained against the 35 that lost. ETERNA (+28.8%), CILEASING (+11.1%) and NEM (+8.7%) were the best-performing stocks while ROYALEX (-15.2%), LIVESTOCK (-10.6%) and ARBICO (-9.6%) led the underperformers.

The Week ahead

We anticipate a continuation of the weak activity level, and a gradual decline of the All Share Index in the short term, especially post interim dividend qualification for the tier 1 banks.

This will ultimately present an even better entry points for Investors, in the run up to 9 Months earnings season, which will indicate what to expect in the full year, in terms of profitability and final dividend.

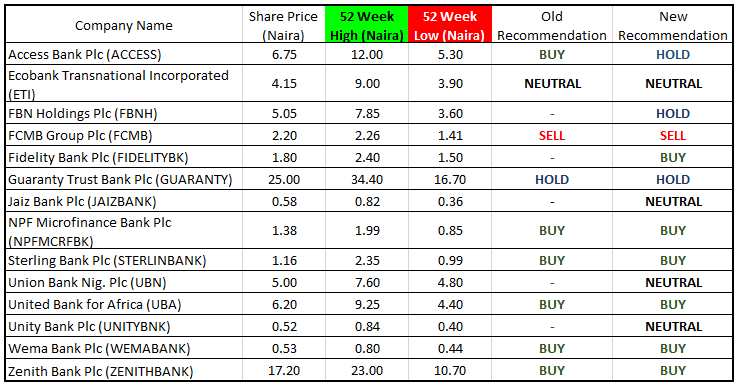

Table: Stock Pick for the week ending 18th September, 2020.

Written by;

Nnamdi M.

{kind=link}