We had discussed in preceding weeks, the items of the balance sheet (Statement of Financial Position) and the income statement (Statement of Profit or Loss) in detail. Having gone through that, how much do we understand the real implications of some of the items discussed?

To understand these implications, we will have to prepare financial statement of a company from conception to operations. Other than helping with our understanding of the implications of these items, this exercise will also help us develop a good financial mindset.

There are many activities a company conduct in a year, and so will our friends at Obi & Ada Enterprises. We had introduced Obi and Ada in week 2, and have been using them as our case study for this class.

Obi and Ada, had conceived a business wherein they buy farm produce from the villages, take the items to the city, process the items at their facility and sell to customers in the city.

- Read also; Warren Buffet’s best performing stocks in the past three months is not Apple or Amazon

- Amended Companies and Allied Matters Act Bill 2020 assented by President Buhari

In starting the business, the first business activity will be financing activity, swiftily followed by investing activity. These activities involve the raising of business capital (financing activity), and subsequently the use of the capital raised to establish the business’s operating base (investing activity).

So, let us begin our exercise of preparing the financial statement of Obi & Ada Enterprises. Most financing and investing activities will be reflected on the Balance Sheet, so we start with an empty balance sheet.

![]()

Table 1: An Empty Balance Sheet for Obi & Ada Enterprises

Activity 1:

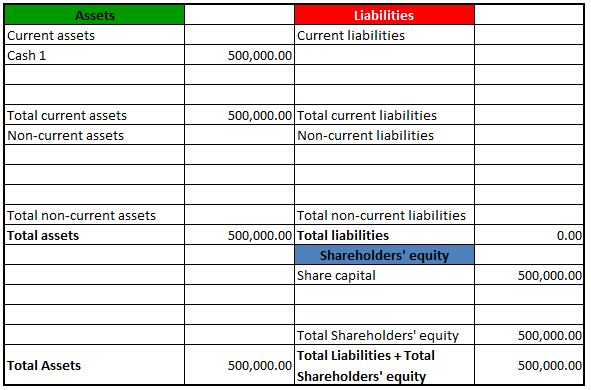

The first activity is to raise capital for the business; for Obi & Ada Enterprises, the capital to start the business is N1,000,000. They pulled capital from their savings, and their relatives invested in the business, all of whom constitute the owners of the new enterprise (Shareholders). The total amount/fund raised by the shareholders is N500,000.

How does this N500,000 get entered into the balance sheet?

Table 2: Activity 1 – Shareholders put in N500,000 into the business

As can be seen in the from table 2 above, the N500,000 was received as “Cash 1” in the current asset column, and also recorded as Share capital signifying that the owners of the company provided N500,000 for business.

The fundamental logic of the balance sheet; Total Asset = Total Liabilities + Shareholder’s equity is maintained.

Activity 2:

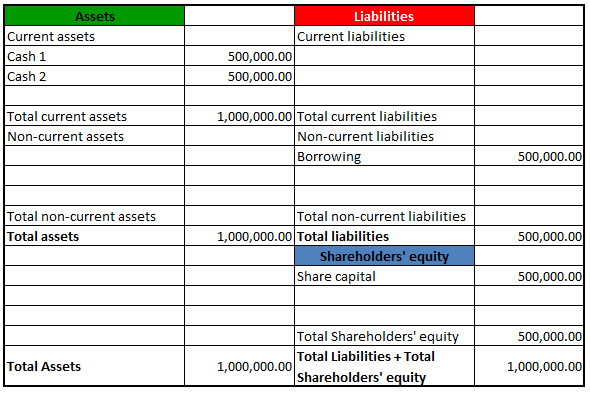

The enterprise needs a N1,000,000 capital to start, but shareholders was able to raise only N500,000. Therefore the company approached the bank for a loan of N500,000 to be repaid in 5 years, to complete the required capital.

How do we record this new cash on the balance sheet?

Table 3: Activity 2 – The company borrows N500,000 from the bank

We can see the new “Cash 2” from the bank reflected on the current asset, while the loan from the bank “Borrowing” for the same amount reflects on the non-current liabilities. It is on non-current liabilities because the company has more than 1 year to repay the loan. Notice also, that the balance sheet logic is still maintained.

Activity 3:

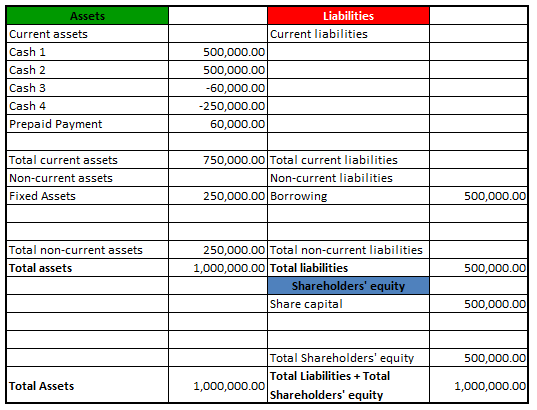

Obi & Ada Enterprises now has enough capital to start its investing activity, and the two founders proceeded to do just that;

- They rented a warehouse in the city and paid N120,000.00 for one year; this is a prepaid payment and will reflect in the current asset. It does not add any new value to the assets, hence it has to be deducted from the total cash (currently at N1,000,000).

- They procured processing equipment, as well as furniture and shelves for their shop. All these constitute fixed assets, and the company paid N250,000 for all these assets.

How do we report this in the balance sheet?

Table 4: Activity 4 – The enterprise invests in fixed assets, and made a prepayment for warehouse space

As we can see, there was no additional cash injection into the business, but the existing cash at the end of activity 2 was used for renting the business premises and also to procure and install fixed assets for the business operations.

Thus at the end of the financing and investing activity needed for the establishment and preparation of the business, what does Obi & Ada Enterprises Balance Sheet look like?

Table 5: The Balance of Obi & Ada Enterprises at the end of the establishment of the business

Note that the fundamental logic of the balance sheet was upheld; Total Assets = Total Liabilities + Total Shareholders’ equity.

Having established the business, and prepared it for operations, the company can now proceed with the next business activity, which is operating activity.

It should be recalled that in earlier weeks, we mentioned that these business activities are continuously repeated in the life span of a company, so as the company begins operating activities, it will also be involved in investing and financing activities.

Next week, we will record procurement and manufacturing activities in the financial statements of Obi & Ada Enterprises.

Written by;

Nnamdi M.

{kind=link}