Welcome to today’s class on Financial and Decision Making. Last week, we introduced financial statements, using the Business Journey of our friends Obi and Ada for illustrations.

Obi and Aba were cousins who started a business of buying farm produce from villages, packing and selling them to customers in the city. They called their business Obi & Ada Enterprises.

They had raised some capital and invested in their new company, and now they are planning to open a new store, and expand their supply chain into a new village. Having become operational, their invested principal which was in the form of cash, have become all kind of things.

What are these things that the principal has become? Obi and Ada turns to the balance sheet to help them understand this, and to ascertain whether their principal still maintains its value.

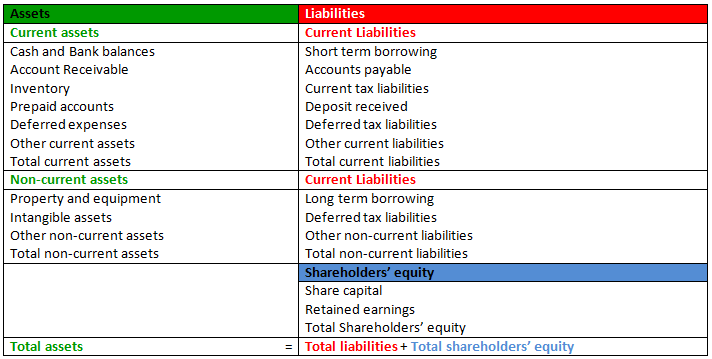

Whether it is called balance sheet or statement of financial position, this type of financial statement will look like the sample shown below.

Fig 1: A Balance Sheet or Statement of Financial Position

The above template follows the International Accounting Standard, and will vary slightly from business to business, and between industrial sectors. Our template has been borrowed from the financial statements of Obi & Ada Enterprises, and will vary in content from that of a company selling building materials or Fashion etc.

- Read also: How much is the Business Worth?

- The International Finance Corporation (IFC): Applying for Financing Part 1

We can see that there are two sides to the balance sheet (statement of financial position); on one side are the Assets, and on the other side is the Liabilities and Shareholders’ equity.

Today, we look at the items on the Assets column, and discuss them so that you as a Business owner can understand which side to place the items while preparing your company’s balance sheet just as they do at Obi & Ada Enterprises.

Before we proceed, it should be noted that the items recorded under current asset (also known as short term assets) are those that can be converted into cash in one year or less; and non-current assets (long term assets) are those that cannot be converted to cash in one year or less.

First item on the asset column is the cash and bank balances, and it is just what it is; in plain terms this is the money the company has at hand and/or deposited in a bank. On some balance sheet, this can be referred to as cash and cash equivalents, when it includes short term securities.

Next on the column is the account receivable AR, or some will write this as trade and other receivables. What is Account Receivable and how is it calculated?

Let us turn to our friends at Obi & Ada Enterprises. The reason they are opening a new shop is to carter for new customers, such as a hotel on the other side of town. To be able to supply the goods to this hotel, they agreed to be paid after 30 days of supplying the goods and issuing an invoice.

Obi & Ada Enterprises having delivered the goods to the hotel, and issued an invoice for the supply, they have a right to receive the payment after 30 days. This right is called accounts receivable. All such outstanding payments the company is waiting to receive is added up, and recorded as account receivable on the balance sheet.

Selling goods on credit is a common phenomenon every business owner or companies deal with on a regular basis, now you know how to record this on your balance sheet.

Inventory! Obi & Ada Enterprises buys farm produce like coconut from the village in bunches, takes it to the city, where they process and sell to their customers as coconut oil, coconut milk, coconut chips etc. When they want to record their inventory, this will include the coconut as bought it from the village, those being processed into different products, as well as finished products.

They will add up the monetary value of the coconut in the various stages, along with their other products and record the total value under inventory.

The next item on the column is prepaid accounts, which is also a common practice seen in many businesses. On her last visit to village to procure some farm produce, Ada discovered that there is insufficient supply of coconut to the market, so to ensure that the company does not suffer unavailability of this item in their shops, she made some cash deposit to the company supplier to secure coconuts coming to the market in advance for them.

This advance payment, or prepayment has bought the company the right to receive inventory from the vendor, and therefore is also an asset. These advancement payments, prepayments or deposits, whatever may be the common term in your area, is added up and recorded under prepaid accounts on the asset column.

We have seen prepaid accounts, where Ada made some deposit for coconuts that will be taken delivery of in the future, but which one are deferred expenses?

Let us consider that Obi has bought some office stationaries that they will use for the next one year, and kept it in the company stores. How will the company should record this; is it as expenses or as an asset?

Let us consider a simple way of differentiating an asset from an expense, after all both of them involves spending of cash today. If the cash spent brings back something that is useful in the future, we can consider it to be an asset, but if it brings back nothing of value in the future, then we consider it as an expense.

Now, let us go back to the office of Obi & Ada Enterprises to see how they dealt with this question. Obi had bought stationaries worth N60,000.00 which they will use for the one calendar year. Under normal circumstances, they use only N5,000.00 worth of stationaries per month.

At the end of the end of the first month, they had N55,000.00 worth or stationaries left, so what they would do is to record N5,000.00 as an expense in the Income Statement (We will address this in later classes) at the end of each month, and the remaining amount as an asset under deferred expenses in the balance sheet.

This scenario can also be seen in other areas, like payment of rent for the shop for one year, payment of advertisement that will run into the future, payment for professional services over a period of time like legal, accounting, auditors etc., all these are calculated the same way as we did for the stationaries and recorded as deferred expenses.

- Further read: Barr. Amaka discusses Nigeria’s Business Laws and Tax System: What every Business Owner should Know – Part 6

While starting the company, Obi and Ada had spent some of their principal to acquire a truck for hauling their raw materials from the village to the city, bought some processing equipment, set-up the store and offices with furniture amongst other things; where should these be recorded?

All the examples mentioned above are fixed, and used in the production process, and are not consumed quickly. It will take years to deplete its entire value. We therefore record them as Property and Equipment or some would call them fixed assets. Fixed assets depreciate over time, and we record depreciation in the income statement to capture the loss of value of the fixed assets.

In the process of developing their products, Obi & Ada Enterprises may have taken out some patents on a new way of packaging coconut they invented, had some copyrights, and proprietary technology on how coconut chips are made etc., all these can be valued and recorded under Intangible assets.

Having identified the asset items in the balance sheet of Obi & Ada Enterprises, do you know how these assets are valued?

We will address that question in our next class.

Written by:

Nnamdi M.